Serving Clients Off the Island? You May Be Leaving Money on the Table

There is a persistent and costly myth in Puerto Rico: that Act No. 60-2019, as amended, known as the Puerto Rico Incentives Code (“Act 60”), is a tax break reserved for wealthy foreigners. Local business owners hear “tax incentives” and assume the conversation isn’t about them. So they keep paying full freight, year after year, while a tool built largely for them sits unused.

The numbers tell a different story. Roughly 65% of Act 60’s incentives are dedicated to Puerto Rico’s own economic development, and more than 60% of all decrees granted over the last 27 years have gone to Puerto Rican entrepreneurs. The most popular of these, by a wide margin, is the Export of Services decree (formerly Act No. 20-2012, as amended). It currently draws the highest volume of decree applications at the Department of Economic Development and Commerce (DDEC).

If you provide a service from Puerto Rico to clients located outside the island, this chapter was written with you in mind.

What “Export of Services” actually means

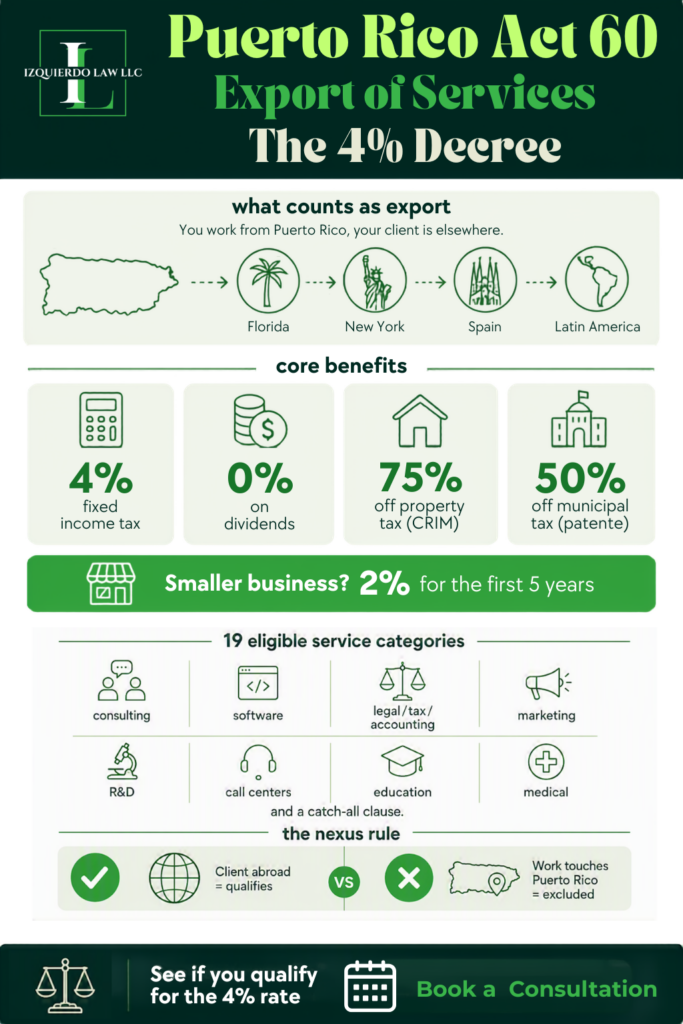

The phrase sounds technical, but the idea is simple. You are exporting a service when you perform it from Puerto Rico for a client located somewhere else. Your office, your team, and your work stay on the island. Your customer are in the US (think Florida, Texas, New York), Virgin Islands, Spain, Latin America, or anywhere beyond Puerto Rico.

That’s it. You don’t ship a product. You don’t open a foreign branch. You simply do what you already do, for clients who happen to be elsewhere.

The rule that matters most: the 4% rate applies only to income generated from Puerto Rico through exported services.

If your business serves both local and international clients, that’s fine. You request a decree covering the export portion of your income, and that portion is taxed at the preferential rate while your local work is treated normally. The condition is recordkeeping: you must maintain books, records, and billing that clearly separate export income, costs, and expenses to the satisfaction of the Treasury Secretary. The 4% rate then applies to the export portion, and your local work is taxed normally.

The benefits: more than just a lower rate

Securing an Export of Services decree is not a one-time discount. It is a contract between your business and the Government of Puerto Rico, carrying constitutional protection and lasting up to 15 years, with the option to renew for another 15 years. Because it is an agreement with the government itself and not with any particular administration, it gives you a stable foundation to plan around for years at a time.

The core benefits include:

-

- 4% fixed income tax rate on income derived from your eligible export activity.

-

- 100% exemption on dividends. Distributions of those earnings to you as the owner are fully exempt.

-

- 75% exemption on real and personal property taxes (CRIM).

-

- 50% exemption on municipal taxes (patente).

For a business owner, the dividend exemption alone can be transformative. It means the profit you pull out of the company to reinvest or pay yourself isn’t eroded a second time.

The PYME advantage: a 2% rate for smaller businesses

Small and medium businesses (“PYME” by its Spanish acronym) have an additional gear. If your business has an average business volume of

$3 million or less over the prior three taxable years and had not begun operations before Act 60 took effect, you may qualify as a “New PYME.” That status lowers the rate from 4% to 2% for the first five years of the decree. During those five years, you also pay 0% in municipal taxes (patente) and 0% in property taxes (CRIM). After year five, the rate steps to 4% and the property and municipal exemptions move to 75% and 50% for the remainder of the decree.

It’s worth understanding that the PYME rate is a modifier applied on top of an Export of Services decree, not a standalone program. You qualify under Export of Services first, then layer the PYME rate on top if eligible.

For a growing company, that is essentially capital you fund your own expansion with, instead of sending it to the government.

Does your service qualify? Probably.

Act 60 lists 19 categories of eligible service activities, and they are broad. They include:

- Research and development. Scientific, technical, or commercial research performed in Puerto Rico for clients elsewhere. Think third-party contract research, contract labs, product testing, and innovation work where the findings are delivered to a company off the island.

- Advertising and public relations. Agencies and consultants that build campaigns, manage media, handle press, and shape reputation for clients located outside Puerto Rico.

- Consulting. One of the broadest categories. It expressly covers economic, environmental, technological, scientific, managerial, marketing, human resources, IT, and audit consulting. Most advisory firms with a defined specialty fit somewhere here.

- Advisory services on any industry or business. A catch-all within consulting. Where category 3 names specific disciplines, this covers advisory work on matters tied to any industry, giving room for niche or cross-disciplinary advisors.

- Creative industries. It reaches ticket sales made outside Puerto Rico (or bought by tourists here), transmission and recording rights sold to audiences off the island, musical productions, and eSports and Fantasy League events held in Puerto Rico. This is the category built for entertainment, media, and content producers.

- Construction blueprints, engineering, architecture, and project management. Design and technical services for projects, including the drawings themselves and the management of the project, performed for external clients.

- Professional services. Specifically legal, tax, and accounting. A Puerto Rico law firm or CPA serving mainland or foreign clients exports under this category, as long as the work doesn’t touch Puerto Rico (more on that limit below).

- Centralized management services. Strategic direction, planning, distribution, logistics, and budgeting run out of a company’s headquarters or regional offices. It also explicitly covers strategic and organizational planning of processes, distribution, and logistics for persons outside Puerto Rico. This is the “regional HQ on the island” category.

- Electronic information processing centers. Facilities that process data electronically, the back-office data operation serving an off-island business.

- Software development. Building computer programs and its service related support. Particularly it can includes bespoke, custom, project-based dev work performed for an off-island client. Note this is the export version. It’s important to note that software development is also available under Manufacturing Chapter 6 that covers local and foreign customers but requires narrower and more product-shaped. The statute requires software or applications that are “licensed or patented” and “reproducible at commercial scale,” where the user interacts with the program to perform specific value tasks, and the revenue comes from licensing, subscriptions, or service charges. That describes a productized, replicable software product (a packaged app or a scalable SaaS), not one-off consulting hours.

- Distribution and licensing income. Distribution done physically, over the internet, via cloud computing, or through blockchain, plus the income from licensing, software subscriptions, or service charges. This is where SaaS and digital licensing models live.

- Telecommunications. Voice, video, audio, and data transmission to persons located outside Puerto Rico.

- Call centers. Inbound or outbound contact center operations (calls, emails, video, etc) serving clients abroad.

- Shared services centers. A back-office hub handling accounting, finance, tax, audit, marketing, engineering, quality control, HR, communications, data processing, and similar centralized functions. Similar in spirit to category 8 but framed around the shared-services operating model.

- Educational and training services. Instruction, course development, and training programs delivered to students or organizations off the island. This can be used and mixed with consulting for coaching programs.

- Hospital and laboratory services. Includes medical tourism and telemedicine facilities. This is the category for clinics and labs serving patients who come from, or are located, outside Puerto Rico.

- Investment banking and other financial services. Asset management, alternative investments, private equity, hedge funds, capital pools, securitization trusts, and escrow administration. Important statutory limit: the law conditions this category on the services being provided by foreign persons, so it isn’t a clean fit for every local financial operator. This one warrants careful structuring.

- Marketing centers. Operations providing space and services such as secretarial, translation, information processing, communications, marketing, telemarketing, and consulting to companies outside Puerto Rico, including export and marketing companies, commercial consulates, foreign-trade agencies, barter operations, and product exhibition centers.

- The catch-all clause. Any other service the DDEC Secretary, in consultation with the Secretary of Treasury, decides should be treated as eligible. The decision weighs whether favorable treatment serves Puerto Rico’s economic and social welfare, the external demand for the service, the number of jobs created, the payroll, the investment the applicant would make, and any other factor deserving special consideration. This is a discretionary petition, not an automatic right, which is why the strength of the legal argument carries real weight. This is exactly where experienced counsel earns its keep. A well-argued petition can bring a service under the decree even when it isn’t explicitly named, which matters as new digital and professional services emerge faster than any statute can list them.

Think of these categories as a buffet, not a single dish. You are not forced to choose just one. A single Export of Services decree can cover every eligible service line your business runs, so a company that does consulting, marketing, and software development can list all three and apply the 4% rate across the board. Act 60 is interpreted in favor of the applicant, and unless the law sets a specific limitation, eligible activities can be combined rather than carved apart. The practical move is to map everything your business does, capture each activity that qualifies, and build them into one decree, while remembering that each service line still has to independently pass the export and Nexus test described below.

The Nexus Rule: The Test That Actually Decides Your 4% Rate

Most people focus on whether their service appears in the list of 19 categories. But fitting a category is only half the test. The other half, and the one that trips businesses up, is Nexus (Nexo).

For income to qualify for the 4% rate, the service has to be a true export from Puerto Rico. That is defined three ways. First, the service must benefit a foreign person, or a non-resident trust or estate, or a Puerto Rico business whose own client is foreign. Second, that the services be offered from Puerto Rico, this is particularly important for the income to be considered Puerto Rico sourced and IRC Section 933 to apply. Third, and just as important, the service must have no Nexus with Puerto Rico.

Nexus means any connection to Puerto Rico. The statute spells out what counts:

-

- Local business activity. Services tied to business or income-producing activities that have been or will be carried out in Puerto Rico.

-

- Advising on Puerto Rico law. Counsel on Puerto Rico statutes, regulations, administrative procedures or rulings, and the precedents of Puerto Rico courts.

-

- Lobbying. Any direct or indirect contact with Puerto Rico government officials intended to influence a government action or determination.

-

- Property used here. The sale of any property for use, consumption, or disposition in Puerto Rico.

-

- A catch-all. Any other activity or circumstance connected to Puerto Rico that the DDEC Secretary designates by regulation or administrative pronouncement.

The practical consequence: a service can sit squarely inside one of the 19 categories and still fail. A Puerto Rico law firm exporting legal services qualifies when it advises a Texas client on Texas matters, but the moment that work turns to Puerto Rico law, that piece has a Nexus and falls outside the decree. The category didn’t change. The Nexus did.

Two nuances that often get missed

Promoter Services are an exception. The statute allows qualifying Promoter Services to be treated as export services even when they have a Nexus with Puerto Rico. This is a deliberate carve-out and a reason to look closely at how a project is characterized.

Professional licensing is relaxed, with a catch. Ordinary Puerto Rico professional-licensing requirements do not apply to an eligible business or its owners and staff, as long as the services are not provided to domestic (Puerto Rico) persons. This also applies to law firms if the owners are in Puerto Rico, per the Ethics Rule 5.5(f) but the owner must be in Puerto Rico exporting the services. The flip side: you still have to comply with the licensing rules of the jurisdiction you are exporting into.

Why work with Izquierdo Law

Qualifying for the 4% rate is rarely a matter of filling out a form. It takes judgment to determine which of the 19 categories fits your operation (and how they could be stacked), how to structure a decree when you serve both local and international clients, whether the PYME modifier applies, and how to keep your benefits protected through annual compliance.

At Izquierdo Law, we help local business owners identify exactly which incentives apply to their specific operations and stay in full compliance so those benefits hold. The decree is a contract, and we make sure you hold up your end while capturing everything the law allows.

If you are serving clients outside of Puerto Rico, you may already be doing the hard part. The next step is making sure you aren’t overpaying for the privilege.

Stop leaving money on the table. Book a consultation with Izquierdo Law to see whether you qualify for the 4% rate.

Disclaimer: This content is for informational purposes only and is not legal advice. Tax incentive eligibility depends on your specific facts. Consult a licensed attorney to evaluate how Act 60 applies to your business.